Yahoo Movies

Yahoo Movies Here's why the stock market's recent selloff has been particularly bad

In what's supposed to be “the most wonderful time of the year,” U.S. stocks have been crushed during the first few weeks in December, erasing this year's gains and tracking to post the first down year since the financial crisis.

One of the under-appreciated explanations intensifying this month's dramatic sell-off is money managers helping clients offset the tax liability from profitable trades by selling money-losing positions, according to a new note from Nick Colas at DataTrek.

"In a few days your clients will see a year-end statement with declining bond, stock, and commodity asset prices. Pretty much nothing worked this year… That will sting, but after a decade of gains that is a manageable issue," Colas wrote, "But… Say you sold some large winners earlier this year as stocks began to roll over, perhaps the large-cap Tech names that everyone from hedge funds to retail investors over-weighted until recently. Those were good sales, to be sure, but in a taxable account they create a future liability and your clients will have to cut a large check to the US Treasury in April 2019."

Selling investments at a loss can help reduce that tax bill that comes with realized capital gains.

"Clients understand mark-to-market losses; they can be less forgiving, however, of out-of-pocket tax payments when there is no wealth effect of rising asset prices to soften the blow,” Colas wrote. “Until September, those paper gains were there. Now, they aren’t.”

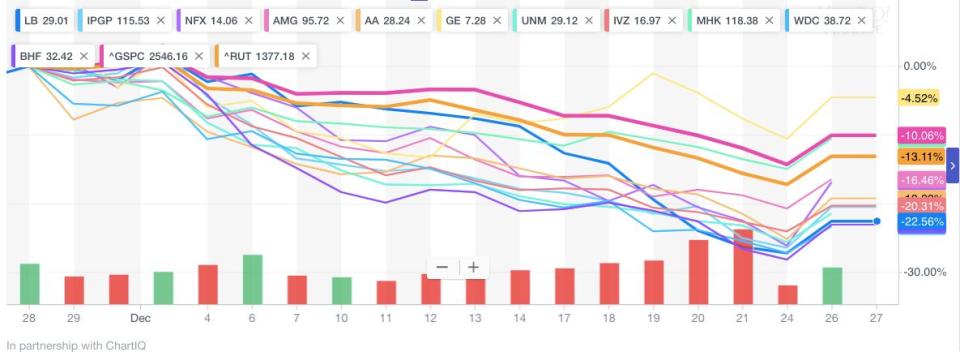

To further illustrate his point, Colas referred to the 11 worst performers in the S&P 500 (^GSPC): General Electric (GE), Mohawk (MHK), Newfield (NFX), Affiliated Managers (AMG), Invesco (IVZ), Western Digital (WDC), L Brands (LB), Alcoa (AA), Unum (UNM), Brighthouse Financial (BHF), and IPG Photonics (IPGP). Excluding GE, those other 10 names were down an average of 22.6% from November 30 through December 24, far worse than the S&P 500's 14.8% decline during that period.

Colas posits that investors motivated by tax planning increasingly dumped these losers.

"These 11 names didn’t suddenly show even-worse fundamentals in December; tax loss selling must have played roll in their dramatic underperformance,” Colas wrote.

However, the tax loss selling may be nearing the end, with those 11 names climbing an average 6.8% during Wednesday's rally.

The potential bright side is the tax loss stock selling in December could open up some buying opportunities in January.

"The big questions just now, made more pointed by [Wednesday’s] rally: is tax loss selling done, and have markets re-priced to attractive enough levels to keep the momentum going? Our thoughts: The answer to the former is clearly 'Yes' – there are only 3 days left in the year, after all."

Colas further cautioned that "healthy" markets don’t see the Dow rally 1,086 points in single trading sessions.

"Recall that [Wednesday’s] record advance eclipsed the following prior gains: October 13 2008 (936 points, the old record), October 28 2008 (889 points) and March 26 2018 (669 points). In each case, markets chopped around for months after."

Indeed, on Thursday morning, Dow futures (YM=F) were down by more than 400 points.

—Julia La Roche is a finance reporter at Yahoo Finance. Follow her on Twitter.