Yahoo Movies

Yahoo Movies Kulicke and Soffa Industries, Inc. (NASDAQ:KLIC) Analysts Revised Next Year's Estimates

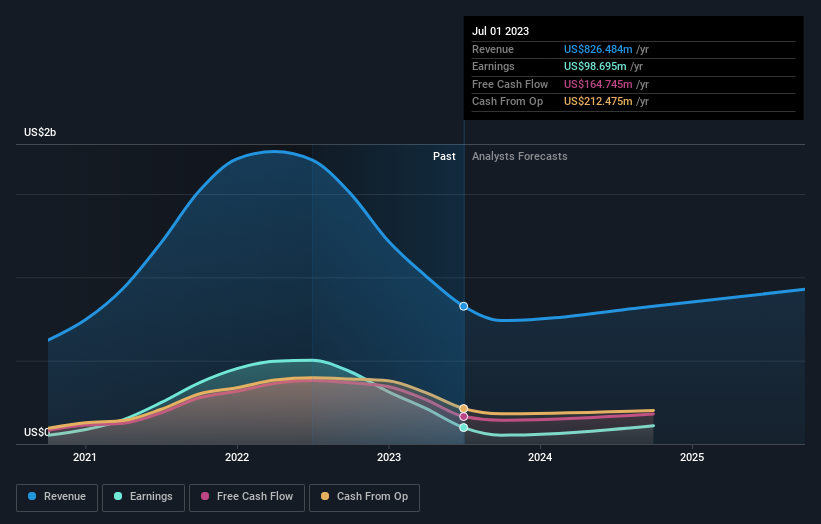

The latest analyst revisions for Kulicke and Soffa Industries, Inc. ( NASDAQ:KLIC ) entail downward adjustments to next year's projections. Notably, both revenue and earnings per share (EPS) forecasts have been revised downward in comparison to previous analyst predictions for the same period. Previously, the analysts had been modelling revenues of US$928m and GAAP earnings per share (EPS) of US$2.04 in 2024. Following the latest downgrade, Kulicke and Soffa Industries' four analysts currently expect revenues in 2024 to be US$827m, approximately in line with the last 12 months. Statutory earnings per share are anticipated to be US$1.54 in the same period. The adjusted EPS for the year 2024 is estimated at $2.12.

It's worth highlighting that despite these revisions pointing downward, analysts are maintaining their projection that both revenue and earnings per share will outperform the anticipated figures for 2023 (US$740.35m and US$0.85 respectively).

See our latest analysis for Kulicke and Soffa Industries

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Kulicke and Soffa Industries' revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 0.01% growth on an annualised basis. This is compared to a historical growth rate of 16% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 14% annually. Factoring in the forecast slowdown in growth, it seems obvious that Kulicke and Soffa Industries is also expected to grow slower than other industry participants.

The Bottom Line

Analysts cut their GAAP earnings per share and revenue estimates compared to the previous consensus. Unfortunately, industry data suggests that Kulicke and Soffa Industries' revenues are expected to grow slower than the wider market. However, it's worth highlighting that despite the downward revisions, both revenue and EPS are still anticipated to exceed the projected figures from the previous year. In light of all of this, it's understandable if investors approach Kulicke and Soffa Industries more cautiously following the recent downgrade.

Our automated valuation tool also suggests that Kulicke and Soffa Industries stock could be overvalued following the downgrade. Shareholders could be left disappointed if these estimates play out. Learn why, and examine the assumptions that underpin our valuation by visiting our free platform here to learn more about our valuation approach.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying .

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.