Yahoo Movies

Yahoo Movies Companies Like Ideal Power (NASDAQ:IPWR) Are In A Position To Invest In Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. By way of example, Ideal Power (NASDAQ:IPWR) has seen its share price rise 328% over the last year, delighting many shareholders. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So notwithstanding the buoyant share price, we think it's well worth asking whether Ideal Power's cash burn is too risky. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

Check out our latest analysis for Ideal Power

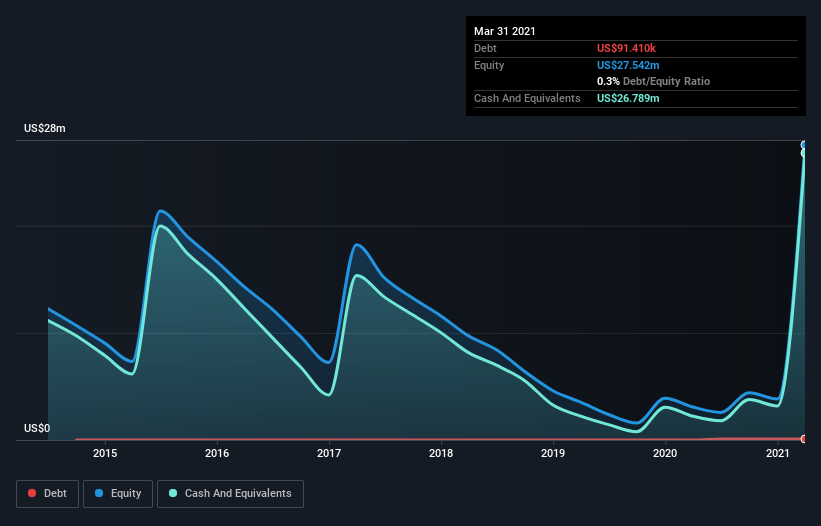

Does Ideal Power Have A Long Cash Runway?

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. As at March 2021, Ideal Power had cash of US$27m and such minimal debt that we can ignore it for the purposes of this analysis. Importantly, its cash burn was US$3.1m over the trailing twelve months. So it had a cash runway of about 8.6 years from March 2021. While this is only one measure of its cash burn situation, it certainly gives us the impression that holders have nothing to worry about. The image below shows how its cash balance has been changing over the last few years.

How Is Ideal Power's Cash Burn Changing Over Time?

In our view, Ideal Power doesn't yet produce significant amounts of operating revenue, since it reported just US$670k in the last twelve months. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. It seems likely that the business is content with its current spending, as the cash burn rate stayed steady over the last twelve months. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Can Ideal Power Raise More Cash Easily?

Since its cash burn is increasing (albeit only slightly), Ideal Power shareholders should still be mindful of the possibility it will require more cash in the future. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of US$51m, Ideal Power's US$3.1m in cash burn equates to about 6.1% of its market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

So, Should We Worry About Ideal Power's Cash Burn?

As you can probably tell by now, we're not too worried about Ideal Power's cash burn. For example, we think its cash runway suggests that the company is on a good path. Although its increasing cash burn does give us reason for pause, the other metrics we discussed in this article form a positive picture overall. Looking at all the measures in this article, together, we're not worried about its rate of cash burn; the company seems well on top of its medium-term spending needs. Taking a deeper dive, we've spotted 4 warning signs for Ideal Power you should be aware of, and 2 of them shouldn't be ignored.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.