Yahoo Movies

Yahoo Movies When to claim on private health insurance – and when to pay up yourself

As the NHS backlog hits new heights, more and more patients are turning to the private sector for their care.

Private elective surgeries, in particular, have seen a big boost in popularity.

The number of self-funded hip replacements rose by 184pc between 2019 and 2022, according to the Private Health Information Network, while private hospitals overtook NHS hospitals for the number of joint operations performed last year.

Whether you need a knee replacement, cancer treatment or a tummy tuck, there is more than one way to access private healthcare in the UK.

Taking out private health insurance is one option, offering peace of mind for a fixed monthly fee.

Alternatively, going without insurance and being prepared to pay for a procedure if you need it will give you more flexibility, but at a higher price.

Balancing the financial risks of each can be daunting. Here, Telegraph Money explains how to weigh up the pros and cons.

What does private health insurance cover?

The conditions covered and the way care is accessed can vary substantially depending on the health insurance policy.

However, basic plans typically cover major surgery when you are admitted to hospital as an inpatient or day patient. You will usually need to be diagnosed via the NHS or required to pay yourself before receiving treatment privately.

Comprehensive policies will include a level of outpatient cover, so you can have tests, scans and pre-diagnosis consultations done privately at a much-reduced cost, as well as inpatient or day patient care.

Chris Steele, a healthcare expert at consumer healthcare information website myTribe, said: “You can tailor your private health insurance policy to include a broader range of treatments and services.

“Outpatient coverage offers many of the main benefits of private health insurance, including consultant appointments, diagnostic tests and outpatient treatments such as physiotherapy.

“Other optional extras include cover for therapies and additional mental health treatment. If you want to improve your core coverage, you can also add extra treatment sessions or increase the financial limits on different types of treatment.”

Jim Easton, chief executive of healthcare company Practice Plus Group, said the questions you need to consider when choosing health insurance are similar to any insurance product.

He said: “How comprehensive is the cover? Does it cover the sorts of things I’d expect? What would I be expected to pay for, like excesses?

“What is the process by which I access care? Do I have complete freedom of choice about where I go to receive care?

“Or, actually, will I be in a situation where I pay a little less for my insurance but I may be more limited in where I can go for my care and who I can see?

“These are perfectly legitimate trade-offs that we all make with insurance, but it’s really worth people making sure they understand what they are.”

The most important point to bear in mind when considering private health insurance is that policies almost never cover pre-existing conditions. If you do have pre-existing conditions, the options will be extremely limited.

Mr Easton adds: “It’s a general truth that insurance is tricky for people with pre-existing conditions. Many with pre-existing conditions will already have experienced this with travel insurance.

“People need to be really aware and careful on the pre-existing conditions point. That’s a fundamental in medical insurance.

“Patients should talk to their insurers, and there are ways around it, but generally it’s hard to insure for pre-existing conditions.”

Pre-existing conditions are defined as conditions for which a patient sought medical advice or treatment in the five years prior to taking out private medical insurance.

Chronic conditions are also excluded. These are illnesses such as diabetes, asthma, arthritis, epilepsy, chronic fatigue, and high blood pressure that doctors cannot cure with a single course of treatment and need long-term management and monitoring.

Mr Steele adds: “Private healthcare only treats short-term acute conditions, so you’ll need to stick with the NHS if you have a chronic illness.

“Depending on the type of underwriting you have with your policy, your insurers may ask you to provide details of your medical history when you sign up for your private health insurance.

“Alternatively, your insurers may investigate to ensure the treatment you need is covered when you claim.”

How much can I expect to pay for private medical insurance?

Like all insurance, healthcare premiums will vary substantially depending on your risk profile, determined in large part by your age and medical history.

Mr Steele said: “Typically, when you take out health insurance you are given a 65 to 70pc no claims discount on day one. Then, if you claim, the discount reduces, sometimes by quite a lot, and your premiums rise.

“Other factors affect premiums too, like your age, and where you live, alongside the claims the insurer has had that year and underlying cost of treatments and medical inflation.”

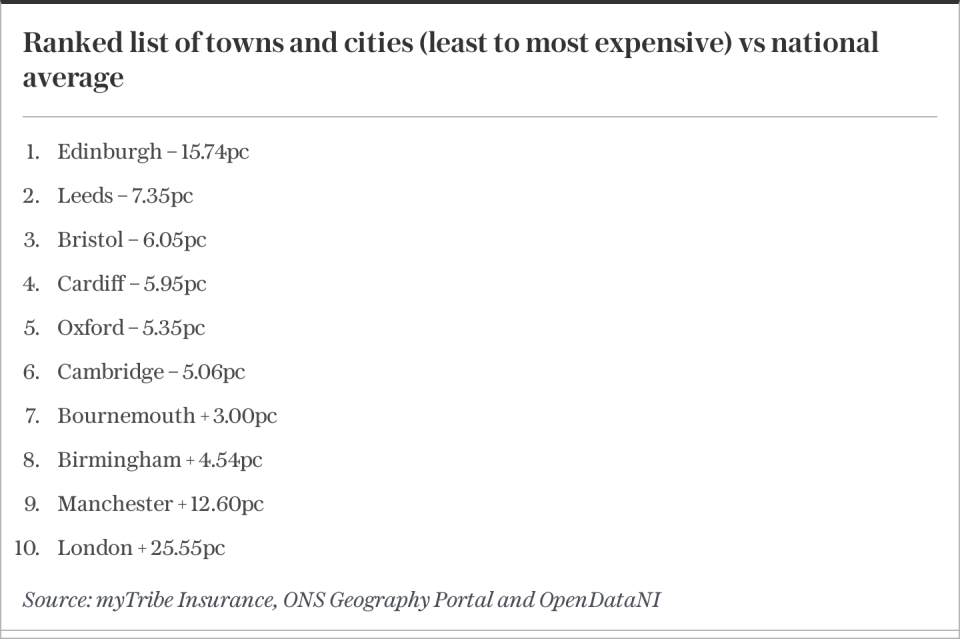

Below are average monthly insurance premiums, separated by age, based on a non-smoker living in Oxford with a maximum excess of £250.

Because premiums are determined in part by the cost of treatment in private hospitals and clinics close to you, the claim rate of your postcode, how affluent your area is, and how many policyholders there are in your area, there is also variation in the average price of cover between regions.

How much do self-pay private operations cost?

Paying for your own care means you have perfect freedom to select which private clinic and consultant you would like to carry out your treatment.

The inevitable drawback is that the option involves paying large lump sums for the privilege.

Mr Steele said: “You don’t need to have private medical insurance to have private treatment. If you have savings, you can also opt to pay your healthcare provider directly.

“If you’ve been diagnosed with a medical condition that can be resolved by surgery, your NHS GP can provide you with a referral letter, or you can choose to pay for a private GP or consultant appointment.

“Your chosen hospital will provide you with a fixed price quote and issue an invoice for payment. Medical loans are also available if you’d prefer to pay in instalments.”

How should I choose between private providers?

With prices for standard procedures often reaching into the tens of thousands of pounds, choosing the right provider that fits with your circumstances is critical.

Mr Easton said: “With self-pay, it’s really worth getting the data, shopping around, looking at quality-metrics, looking at prices.

“If you’re willing to travel for an extra 30 minutes you may find there’s high quality provision at a more attractive price.

“People don’t have to accept the first thing that comes to mind or that they’re offered when it comes to a self-pay option.

“There’s loads of data available to help them make the decision, and most providers will provide most of that on their website. It’s really worth people looking.

“The questions to ask are: How local is it? What do my friends and neighbours say about the reputation (which matters to people)? What’s the probability of my operation going well?

“The overarching source of information is the care quality commission. They will have the data if you’re looking at a local private hospital.”

How should I choose between self-pay and private insurance?

If you want to access healthcare quickly and are facing a long wait on the NHS, funding your own care can offer the best alternative – as long as you have the funds.

If you don’t have health insurance, or it doesn’t cover the procedure or treatment you need, then self-pay may also be the way to go.

Mr Steele added: “The best thing about self-pay in my mind is that there are no exclusions, if you can find the money, you can get the treatment.”

There are three key reasons that might tilt the balance in favour of self-pay, according to Mr Steele.

Your treatment is low-cost

“The cost of private surgery varies depending on what you need. Some procedures, such as cataract surgery, a tonsillectomy or a colonoscopy, cost in the region of £1,500 to £2,775,” he said.

“Others cost a lot more, with knee surgery or a hip replacement costing in the region of £12,000 to £13,000. However, if you have the means, you may consider it worth the cost if it helps you regain your quality of life.

“Your views on what represents a low-cost treatment will depend on your circumstances and how much you have tucked away in savings.”

You want a quick diagnosis

“If you want to see a consultant quickly or have diagnostic scans and tests privately, these will typically cost a few hundred pounds. The cost could be well worth it if it helps you to spend less time on an NHS waiting list.

“Even if you can’t stretch to private treatment, this could help you to get the care you need more quickly.”

Your health insurance doesn’t cover your treatment

“You may already have private health insurance but find that it doesn’t cover your treatment, either because you don’t have the right level of coverage or because of an exclusion on your policy.

“For example, you might have chosen private medical insurance to cover inpatient treatment and surgery or private treatment if you’re diagnosed with cancer but found that outpatient coverage took the cost of your medical insurance beyond your budget.

“If you don’t have outpatient coverage, you won’t be able to get a private diagnosis, but you can get a referral from your GP for private healthcare after being diagnosed via the NHS.

“If you’ve seen your GP and received a referral to a consultant, private health insurance won’t cover your treatment as your insurer will class it as a pre-existing condition. That means you’ll need to wait for NHS treatment or fund your own private healthcare.”

Mr Easton added: “One of the most important things to consider is what pre-existing conditions you have. If you have heart disease, previous cancer, that sort of thing, you’re going to struggle to get insurance that covers those things.

“Healthcare can get very expensive very quickly. So whichever route you choose, make sure you have real clarity about what [you’re] going to pay and what it’s for, and whether you have exposure to any other costs.”

What about the NHS?

Accessing treatment on the NHS is becoming increasingly difficult. There were 7.77 million waits for non-emergency care at the end of September, up from 7.75 million in August – a new record high.

Mr Easton said that while the NHS is “particularly slow” at the moment, it still trumps going private in some areas of care.

He added: “Across nearly every metric the NHS is not providing the responsiveness it was five years ago. But you can still get access to good quality cancer treatment and emergency care on the NHS.

“You may wait longer than you would have five years ago for an initial consultation but the metrics still suggest that you will get good quality treatment once you get it.

“If you don’t have pre-existing conditions, that’s the trade-off. Do I want to just have peace of mind and be prepared to pay a premium for that, for rapid access to pretty much everything I want?

“Or, I think the NHS for really serious things is OK, and for those things like hips and knees which are very slow, if those needs arise and I need to top it up [by going private], then I can and that package works for me.

“You’re kind of using the government-insured part – the NHS – and topping that up as required.

“That’s an evaluation people make based on their pattern of disposable income, how they feel about their health, what’s their family history, all those factors.”

How can I best combine NHS treatment with private healthcare?

Combining private and NHS healthcare can often be a pragmatic compromise which strikes a balance between cost and convenience.

For instance, you might choose to receive most of your healthcare on the NHS, but then decide to have surgery in a private clinic to reduce the amount of time it takes to get seen and treated.

This merging of public and private works both ways. Private hospitals will sometimes discharge a patient back to their GP to monitor their progress after a private operation.

Mr Steele said: “If you have health insurance but have either a chronic condition or a pre-existing condition that’s excluded, you can access private healthcare for the things that are covered and NHS treatment for everything else.

“Many health insurance policies also have a cash benefit which pays a fixed amount if you’re treated in an NHS hospital.”

There are two key things to bear in mind when assessing whether to opt for NHS or private medical care.

The first is that the NHS is the best bet in an emergency. “If you need to go to A&E, you won’t find it at a private hospital as most private hospitals don’t offer emergency care.

“Some provide a private urgent care service which will allow you to be seen and treated on the same day, but you need to make an appointment.

“They will still tell you to go to A&E if you’ve been in a serious accident, have severe bleeding or think you’re having a heart attack or stroke.

“Receiving NHS care in an emergency means you’ll have access to specialist doctors who can manage your treatment after you’ve received emergency care.”

The second is that chronic conditions are usually best dealt with through the NHS. Mr Steele adds: “If you have a chronic condition such as asthma or diabetes, you’ll need ongoing health monitoring and management.

“That falls within the NHS’ remit, mainly because health insurance doesn’t cover chronic conditions.

“With NHS care, you’ll benefit from an ongoing relationship with your GP, who’ll get to know you and provide you with the care that’s tailored to your needs.”

Recommended

Care home fees are rising – find out the costs, and how to get funding