Yahoo Movies

Yahoo Movies Is Ekso Bionics Holdings (NASDAQ:EKSO) Weighed On By Its Debt Load?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Ekso Bionics Holdings, Inc. (NASDAQ:EKSO) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Ekso Bionics Holdings

What Is Ekso Bionics Holdings's Debt?

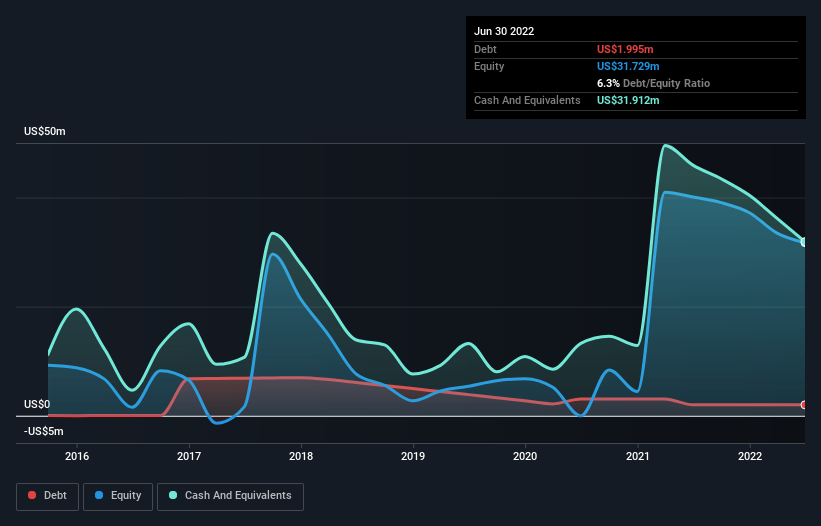

The chart below, which you can click on for greater detail, shows that Ekso Bionics Holdings had US$2.00m in debt in June 2022; about the same as the year before. However, its balance sheet shows it holds US$31.9m in cash, so it actually has US$29.9m net cash.

How Strong Is Ekso Bionics Holdings' Balance Sheet?

According to the last reported balance sheet, Ekso Bionics Holdings had liabilities of US$4.82m due within 12 months, and liabilities of US$3.97m due beyond 12 months. On the other hand, it had cash of US$31.9m and US$3.34m worth of receivables due within a year. So it can boast US$26.5m more liquid assets than total liabilities.

This surplus strongly suggests that Ekso Bionics Holdings has a rock-solid balance sheet (and the debt is of no concern whatsoever). On this view, lenders should feel as safe as the beloved of a black-belt karate master. Simply put, the fact that Ekso Bionics Holdings has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Ekso Bionics Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Ekso Bionics Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 42%, to US$13m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Ekso Bionics Holdings?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Ekso Bionics Holdings had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$14m and booked a US$12m accounting loss. Given it only has net cash of US$29.9m, the company may need to raise more capital if it doesn't reach break-even soon. With very solid revenue growth in the last year, Ekso Bionics Holdings may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for Ekso Bionics Holdings you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here