Yahoo Movies

Yahoo Movies Public Storage (NYSE:PSA) Stock's Been Sliding But Fundamentals Look Decent: Will The Market Correct The Share Price In The Future?

With its stock down 2.1% over the past three months, it is easy to disregard Public Storage (NYSE:PSA). However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. In this article, we decided to focus on Public Storage's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

Check out our latest analysis for Public Storage

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Public Storage is:

17% = US$1.4b ÷ US$8.5b (Based on the trailing twelve months to September 2020).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each $1 of shareholders' capital it has, the company made $0.17 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Public Storage's Earnings Growth And 17% ROE

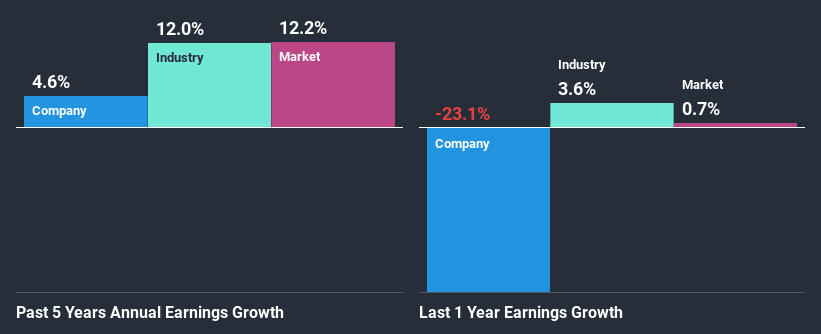

At first glance, Public Storage seems to have a decent ROE. Especially when compared to the industry average of 5.5% the company's ROE looks pretty impressive. Yet, Public Storage has posted measly growth of 4.6% over the past five years. This is interesting as the high returns should mean that the company has the ability to generate high growth but for some reason, it hasn't been able to do so. We reckon that a low growth, when returns are quite high could be the result of certain circumstances like low earnings retention or poor allocation of capital.

As a next step, we compared Public Storage's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 12% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Has the market priced in the future outlook for PSA? You can find out in our latest intrinsic value infographic research report.

Is Public Storage Making Efficient Use Of Its Profits?

Public Storage seems to be paying out most of its income as dividends judging by its three-year median payout ratio of 89% (or a retention ratio of 11%). However, this is typical for REITs as they are often required by law to distribute most of their earnings. Accordingly, this suggests that the company's earnings growth was lower as a result of the high payout.

Moreover, Public Storage has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to drop to 68% over the next three years. The fact that the company's ROE is expected to rise to 23% over the same period is explained by the drop in the payout ratio.

Summary

On the whole, we do feel that Public Storage has some positive attributes. However, while the company does have a high ROE, its earnings growth number is quite disappointing. This can be blamed on the fact that it reinvests only a small portion of its profits and pays out the rest as dividends. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.